Losing a loved one is never easy. Amidst the emotional upheaval, the burden of managing financial matters—especially filing a life insurance claim—can feel overwhelming. For nominees, this is often uncharted territory, made harder by grief and uncertainty. Understanding the steps involved in the claims process can ease some of this strain. Knowing what to expect, what documents are needed, and how long the process may take can bring a small sense of control during a deeply challenging time.

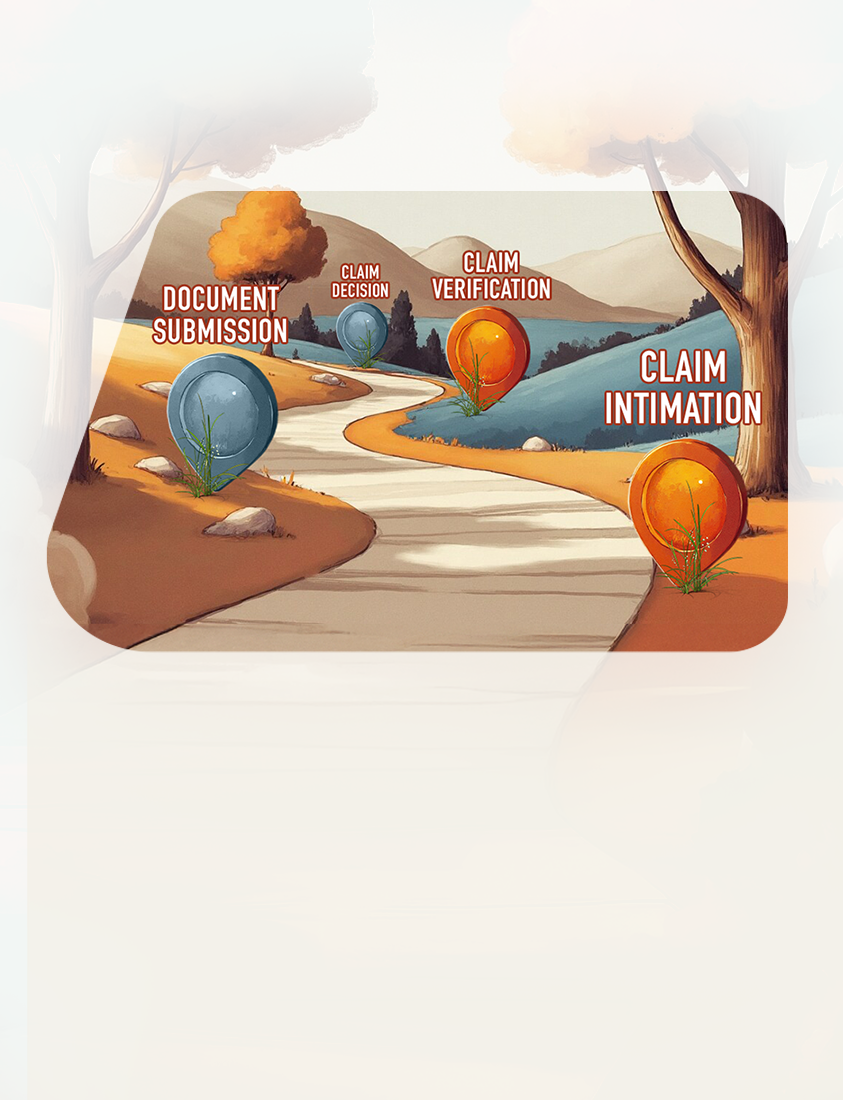

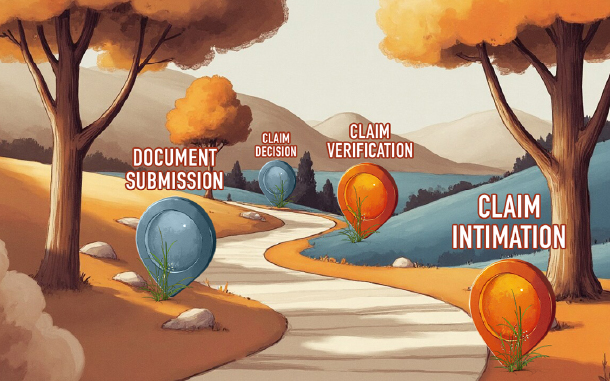

Step 1: Claim Intimation

The first step in the Life Insurance Claim Process is claim intimation—formally notifying the life insurance company about the policyholder’s death. This responsibility usually falls on the nominee listed in the policy.

The intimation can be done online through the insurer’s website, by calling the customer service helpline, or by visiting the nearest branch. The nominee will need to provide basic details such as the policy number, name of the deceased policyholder, date and cause of death, and their own contact information.

Most insurers have a claim intimation form that needs to be filled out. Some may also ask for a copy of the death certificate at this stage. Prompt intimation ensures that the claim process begins without unnecessary delays, helping the nominee access the policy benefits as soon as possible.

It is ideal to inform the insurer as soon as possible after the death—preferably within 30 days. Early intimation helps speed up the overall claim process.

Step 2: Submission of Documents

Once the claim is initiated, the nominee may need to submit a set of documents. These usually include:

Duly filled claim form

Death certificate (original or attested copy with verifiable QR code)

Original policy document

KYCs of the Life Assured

Identity and address proof of the nominee

KYCs of the Nominee

Bank account details (cancelled cheque or bank passbook copy)

Medical/Hospitalization Documentation (in case of institutional death)

In case of accidental or unnatural death, additional documents may be required:

For NRIs who are nominees, the following must also be provided:

Ensuring all documents are in order and submitting them together helps avoid delays.

Step 3: Claim Verification by the Insurer

After receiving the documents, the insurer begins the verification process. This includes:

Validating the submitted documents

Checking underwriting records

Internal due diligence to rule out any discrepancies

The time taken to verify a claim depends on whether it is an early or non-early claim (varying company wise)

Early claim: If the policyholder dies within three years of the policy issuance, the insurer may conduct additional investigations.

Non-early claim: These are usually processed faster due to the lower risk profile.

As per IRDAI regulations:

For claims requiring investigation, the insurer has up to 45 days from the date of claim intimation with all mandatory documentation.

Step 4: Communication from the Insurer

Once the claim is initiated, the insurer makes it a priority to keep the nominee updated at every important stage. Clear and timely communication is crucial—especially during a time when the nominee may already be dealing with emotional distress and practical uncertainties.

Updates are typically shared through multiple channels, including:

SMS alerts - These provide quick notifications about the progress of the claim, such as receipt of documents or approval status.

Emails - Detailed updates, next steps, and any pending requirements are often communicated via email for easy reference.

Personal calls - In certain cases, especially where sensitive or complex information needs to be shared, the insurer may reach out through a phone call for direct assistance and guidance.

If the insurer needs any additional information, documents, or clarification, they will get in touch promptly. It is important for the nominee to remain attentive and responsive to these communications. Timely follow-ups and cooperation can help ensure the claim is processed smoothly and without avoidable delays.

Step 5: Claim Decision

Once the verification is complete, the insurer may decide whether to approve or reject the claim.

If approved, the insurer proceeds to initiate the payout.

If rejected, the nominee will be informed of the reason in writing. Common reasons include policy in lapse status, incorrect details/non-disclosure, or exclusions applicable to the cause of death.

Nominees who feel the rejection is unjustified can:

Appeal to the insurer’s grievance redressal officer

Approach the Insurance Ombudsman

File a complaint with IRDAI

According to IRDAI guidelines:

Claims without investigation must be settled within 15 days from the date of receipt of all documents.

Claims with investigation must be settled within 45 days from the date of receipt of all documents.

Step 6: Payout

If the claim is approved, the death benefit is paid to the nominee. The amount is usually transferred directly to the nominee’s bank account via:

There are no tax implications for the nominee. As per Section 10(10D) of the Income Tax Act, life insurance death benefits are completely tax-free.

Additional Tips for Nominees

Being a nominee for a close one can be overwhelming and emotionally taxing due to the acknowledgement of their mortality. However, if you’ve has a conversation with the policyholder, you should be ready for the possibility. Here are a few tips that will help you in doing so:

Keep Documents Ready: Gather and preserve all necessary documents, both digital and physical, in one place.

Intimate Early: The sooner the insurer is informed, the smoother the process.

Update Nominee Details: Ensure the policy has correct and updated nominee information to avoid disputes and delays.

Initiating and fulfilling a claim for life insurance policy is usually a straightforward process when the right steps are followed. With proper documentation and timely communication, the payout can be processed swiftly and without complications.

Policyholders should talk to their families about the claim process and share necessary details like policy numbers, insurer contact, and nominee information. Being informed today can make a difficult day a little easier tomorrow.

Feel free to share this guide with your loved ones. It may one day help them navigate a tough time with greater ease and confidence.