The assurance of a life insurance policy lies in the financial protection it can provide to your loved ones. When a loved one passes away; grief is often accompanied by financial uncertainty. Life insurance is meant to offer support during this time—but the process hinges on one important person: the nominee. Despite being listed on almost every policy, many don’t fully understand what a nominee does or how crucial their role is in ensuring a smooth claim process.

Who is a Nominee?

A nominee is the person chosen by the life insurance policyholder to receive the policy benefits in case of the policyholder’s death during the policy term. This could be a spouse, child, parent, sibling, or any other loved one the policyholder trusts.

When Does a Nominee Raise a Claim?

The nominee is required to fully step into their role if the life insured passes away during the policy term. The nominee is expected to initiate a claim to receive the benefit under the concerned policy. This is referred to as a death claim, as the claim process begins after the insurer is informed of the policyholder’s demise. From this point, the nominee is responsible for fulfilling their end of the claim process.

On the other hand, the maturity benefit claim is directly handled by the policyholder. If the policy matures while the policyholder is alive, the maturity benefit is paid directly to the policyholder/life assured. The nominee is not involved in the process.

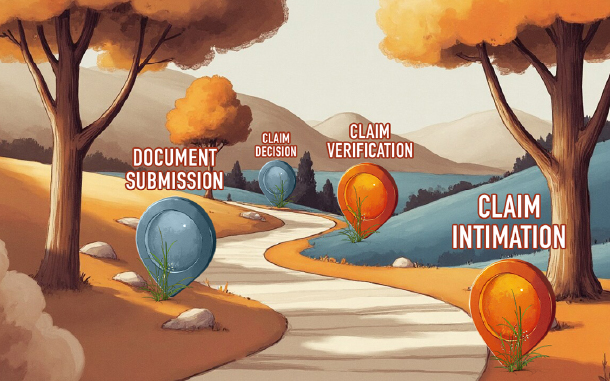

Responsibilities of a Nominee During the Claim Process

The nominee takes on several responsibilities during the claim process to ensure that the process is fulfilled and the benefits are received without any hassles.

-

Informing the Insurer

The first responsibility of the nominee is to intimate the life insurance company about the demise of the policyholder. This should be done as soon as possible. A copy of the death certificate should also be provided to initiate the claim process right away.

-

Collecting and Submitting Claim Documents

After informing the insurer, the nominee must gather and submit all the valid and mandatory documentation as listed /mentioned by the insurer company.

-

Cooperating in the Verification Process

Once the claim is filed, the insurance company will begin its assessment and verification process. The nominee should do their part by cooperating during this stage. This can involve reverting to queries, clearing doubts, submitting additional documents if needed.

-

Receiving the Claim Amount

Once the claim is verified, the insurer will process the claim and release the payout. In most cases, where there are no legal disputes, the claim amount is transferred directly to the nominee’s bank account.

Claim Documents Required from the Nominee

To ensure a smooth claim process, the nominee is usually required to provide the following documents as per the claim filed (the list may vary slightly from company to company):

Original policy document

Original death certificate of the Life Assured with verifiable QR code

KYCs of the Life Assured

Identity/address proof of the nominee

Bank details (cancelled cheque or passbook copy) of the nominee

Nominee declaration form

Medical/Hospitalization documentation (in case of institutional death)

Depending on the details of the case, more documents may be requested. It is ideal to have these documents ready, to avoid delays in claim processing.

Legal Considerations the Nominee Must Keep in Mind

It is quite common for legal issues to arise when it comes to disbursing the life insurance claim proceeds of a deceased individual. However, by being aware of certain legal considerations and keeping them in mind when selecting a nominee, one can avoid such issues from occurring.

-

The Difference Between the Nominee and Legal Heir

One thing to keep in mind is the difference between a nominee and a legal heir. Legally, a nominee is considered a custodian or trustee of the assets in the presence of a legal heir. He/ she is expected to receive the claim amount on behalf of the legal heir, who is named as the inheritor of the deceased person’s assets as per their legal will.

Unless the nominee is also a legal heir, has been designated as the beneficial nominee, or has been given certain rights through a will, they may be required to transfer the funds to the rightful heirs. That is why it is important to address this in advance, to avoid legal disputes in the absence of the policyholder.

-

What Happens if the Will Conflicts with the Nomination

If a will exists that names someone else as the legal heir, chances are the will can override the life insurance nomination. In such cases, the nominee may receive the funds initially. However, they may be legally expected to hand them over to the person named in the will. This is why the policyholder must ensure their life insurance nomination aligns with their legacy planning. It can help avoid complications in the family, which may arise if the nominee and the legal heir dispute over receiving the life insurance proceeds.

Role of a ‘Beneficial Nominee’ (Post-2015 IRDAI Rule)

To address the legal issues arising between nominees and legal heirs, the Insurance Regulatory and Development Authority of India (IRDAI) introduced the concept of a ‘beneficial nominee’ in 2015. As per this concept, if a policyholder nominates a close family member, such as a spouse, parent, or child, they will be treated as the beneficial nominee. This means they are not ‘trustees’ but also legal owners of the insurance proceeds.

As a policyholder and as a beneficial nominee, this rule can give peace of mind as one is assured that the intended person will receive the benefits.

What if the Nominee is an NRI?

If the nominee is a Non-Resident Indian (NRI), the claim process remains largely the same but may require additional documentation. This usually consists of verified copies of the NRI nominee’s passport, visa, and proof of an Indian bank account to receive the funds. Some insurers may have specific requirements or processes for NRI nominees, so it is best to check with the insurer before assigning an NRI as the nominee.

The process of nomination plays a crucial role in ensuring that your life insurance benefits reach your loved ones without delay. If you have not done it recently, take a few minutes today to check and update your nomination. A small step today can make a large difference for your loved ones tomorrow.