Join us as an Advisor

Join us as an Advisor

:

:  :

:  :

:

Patients")

High blood pressure, or hypertension, can be one of the critical health factors insurers evaluate for term insurance eligibility and premium costs. With its potential to increase the risk of heart disease, stroke, and other severe medical conditions, hypertension can complicate the process of getting life insurance coverage. However, with careful management and strategic planning, individuals with high blood pressure can still obtain suitable policies.

How Does High Blood Pressure Affect Term Insurance?

Individuals diagnosed with high blood pressure, or hypertension, often face unique challenges when purchasing term insurance. This medical condition is a crucial factor insurers consider, impacting not only the approval of coverage but also the premium costs.

Blood Pressure Ranges and Insurance Implications

High blood pressure is categorised into four ranges to understand the severity of the condition and its impact on the person’s health and mortality. Based on which category the life assured is diagnosed under may determine the policy benefits they are offered, the customisations they can choose, as well as the premium amount for the policy details chosen.

Here is a quick look at each of these categories and how it may influence their premium amount.

- Normal Blood Pressure (Less than 120/80 mm Hg): Generally, these individuals receive standard premium rates.

- Elevated Blood Pressure (120-129/less than 80 mm Hg): May still qualify for standard rates but face closer inspection.

- Stage 1 Hypertension (130-139/80-89 mm Hg): These applicants often see higher premiums due to the possible risks associated with cardiovascular diseases.

- Stage 2 Hypertension (140/90 mm Hg or higher): Significantly increased premiums and possible denial of coverage, depending on the individual’s health profile.

Using a term insurance calculator can help you understand how blood pressure levels influence premium costs. It can give you a clearer picture of potential financial commitments.

Influence of Age on Premiums for Hypertension Patients

Age is another crucial factor for hypertensive individuals seeking term insurance. Younger applicants with well-managed high blood pressure often receive more favourable rates compared to older applicants whose hypertension might contribute to additional health complications. The interaction between age and hypertension emphasises the importance of starting a life insurance plan early when premiums are generally more affordable.

Why General Health Matters in Term Insurance for Hypertensive Patients

General health significantly impacts insurance eligibility and premiums. Insurers evaluate lifestyle choices, medical history, and ongoing health conditions. Individuals with well-controlled hypertension, due to healthy habits such as regular exercise and a balanced diet, may still qualify for competitive rates. However, untreated or poorly managed hypertension can signal a higher risk of serious health conditions, influencing insurers to impose exclusions or higher costs.

Can You Get Term Insurance with High Blood Pressure?

Securing term insurance for individuals with hypertension is possible, but it often requires strategic planning. Many insurers evaluate applicants based on the stability and management of their condition.

Tips for Securing Term Insurance with High Blood Pressure

- Choose the Right Insurer: Some insurers specialise in providing coverage to people with pre-existing conditions, making it crucial to compare different life insurance options.

- Document Management: Provide thorough medical records detailing how hypertension is managed.

- Review Policies Regularly: As your health improves, review your insurance to potentially lower premiums.

Maintaining Regular Checkups

Regular health checkups help keep blood pressure in check and provide documented proof of stability. It reassures insurers of the applicant’s commitment to maintaining good health. These records may strengthen the case for more affordable term insurance premiums.

Avoiding Blood Pressure-Influencing Substances

Lifestyle adjustments, such as reducing alcohol and tobacco consumption, can positively impact blood pressure levels. Insurers favour applicants demonstrating proactive health management, which can lead to better premium rates.

Best Life Insurance Options for Individuals with High Blood Pressure

People with hypertension may explore various life insurance policies catering to their needs.

Whole Life Insurance

This type of life insurance policy provides lifelong coverage and builds cash value over time. While premiums are higher, it ensures long-term security. Individuals with hypertension may opt for whole life insurance for its guaranteed payout and fixed premiums.

Term Life Insurance

It is a cost-effective option for hypertension patients, offering coverage for a specific duration. With the right management of blood pressure, some can secure reasonable premiums. Comparing multiple term insurance plans is essential to find the best fit.

Guaranteed Issue Life Insurance

For those who struggle to qualify for traditional term insurance due to severe hypertension, guaranteed issue policies are an option. These policies do not require a medical exam but come with higher premiums and lower coverage limits.

Securing term insurance for individuals with hypertension can be more complicated than for those without the condition. However, by understanding the factors influencing premiums and exploring various life insurance plans, you can find suitable coverage. Managing hypertension effectively and choosing the right policy is key to ensuring financial protection.'

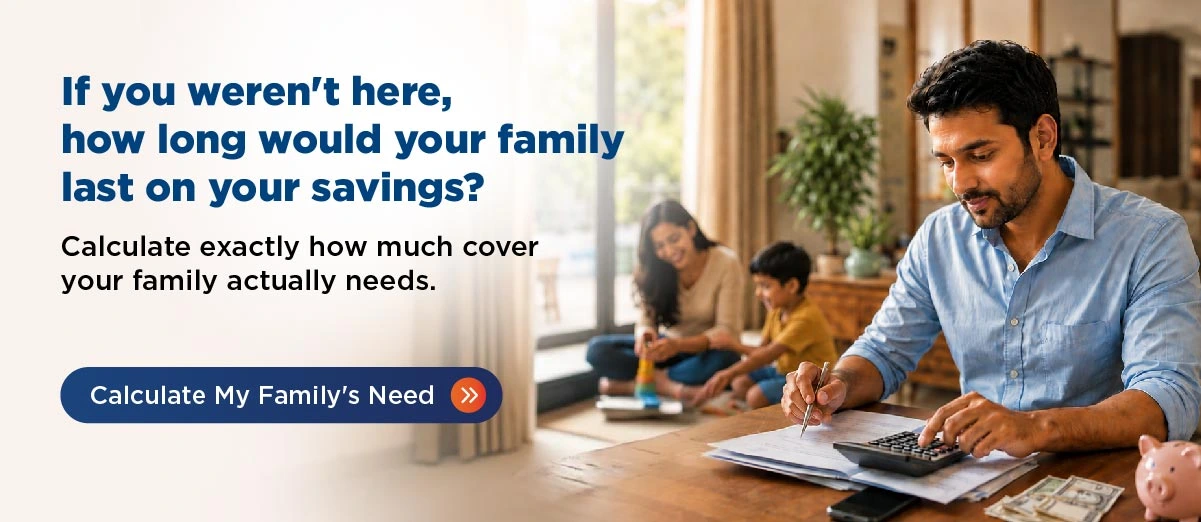

Before You Go

Your family depends on your love, support, and financial security.

Take the first step towards understanding the protection they may need.