Join us as an Advisor

Join us as an Advisor

:

:  :

:  :

:

?")

Key Takeaways

- An SWP allows you to withdraw a fixed amount from your investment at regular intervals while keeping the remaining corpus invested for potential growth.

- SWPs are suitable for retirees, parents, and individuals seeking a regular income stream to meet recurring financial commitments.

- Compared to lump-sum withdrawals, SWPs offer better cash flow management, financial discipline, and continued participation in market-linked growth opportunities.

- In addition to mutual funds, certain ULIPs also offer SWP-like features, helping investors combine regular income, wealth creation, and life insurance protection.

Financial planning is not just about building wealth; it is also about creating a steady income stream when you need it. While many investors focus on accumulating funds through regular investments, there eventually comes a stage when those investments need to generate income. This is where an SWP, or Systematic Withdrawal Plan, becomes relevant.

No matter you are planning for retirement, looking for a supplementary source of income, or seeking a disciplined way to access your investments, understanding what SWP is can help you make informed financial decisions.

Read on to understand what systematic withdrawal plan is, how it works, its benefits, types, taxation, and how it can also be used through life insurance products such as ULIPs.

What is SWP?

A Systematic Withdrawal Plan (SWP) is a facility that allows investors to withdraw a fixed amount from their investments at regular intervals while keeping the remaining amount invested.

If you are wondering what SWP investment is, it is not a separate investment product. Instead, it is a withdrawal mechanism offered by mutual funds and certain Unit Linked Insurance Plans (ULIPs).

Under an SWP, investors can choose:

- The withdrawal amount

- Withdrawal frequency (monthly, quarterly, half-yearly, or annually)

- Start date of withdrawals

The remaining corpus continues to stay invested and can potentially grow depending on market performance.

Example

Suppose you have invested ₹10 lakh in a fund. Instead of withdrawing the entire amount at once, you may choose to withdraw ₹10,000 every month through an SWP. While these withdrawals continue, the remaining balance remains invested and may generate returns.

What is SWP in Investment?

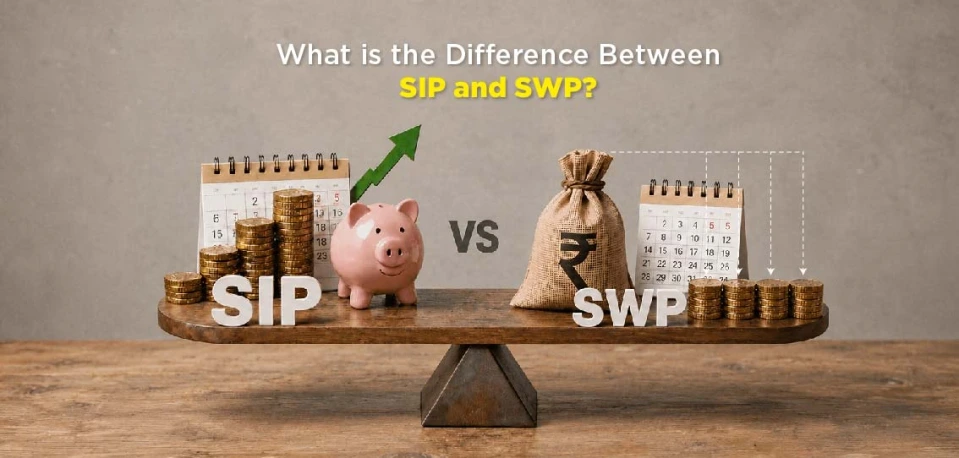

To understand what SWP in investment is, think of it as the reverse of a Systematic Investment Plan (SIP).

SIP | SWP |

Invest money regularly | Withdraw money regularly |

Helps build wealth | Helps generate income |

Suitable during earning years | Suitable during retirement or income-distribution years |

Money flows into investments | Money flows from investments |

While SIP focuses on wealth creation, an SWP focuses on wealth utilisation without liquidating the entire investment corpus.

How Does an SWP Work?

The process of setting up an SWP is relatively straightforward.

Step 1: Build an Investment Corpus

You first invest a lump sum amount in a mutual fund or eligible insurance-linked investment plan.

Step 2: Choose Withdrawal Details

You decide:

- How much money to withdraw

- How often to withdraw

- Duration of withdrawals

Step 3: Automatic Redemption

On each withdrawal date, units equivalent to the withdrawal amount are redeemed from your investment.

Step 4: Amount Credited

The redeemed amount is transferred directly to your bank account.

Step 5: Remaining Funds Continue Growing

The remaining units stay invested and continue participating in market growth.

This mechanism makes the SWP fund approach attractive for investors who need regular income while maintaining exposure to long-term growth opportunities.

Types of SWP Plans

Understanding what SWP plan is also involves knowing the different withdrawal options available.

1. Fixed Amount SWP

A predetermined amount is withdrawn at regular intervals.

Example: ₹15,000 every month.

2. Appreciation SWP

Only the gains generated by the investment are withdrawn, while the principal remains invested.

This option may help preserve capital for a longer period.

Benefits of a Systematic Withdrawal Plan

A systematic withdrawal plan offers several advantages.

1. Regular Income Stream

SWPs can provide predictable cash flow for:

- Household expenses

- Utility bills

- Medical expenses

- Loan repayments

2. Continued Market Participation

Unlike lump-sum withdrawals, most of the corpus remains invested, enabling potential wealth growth.

3. Better Cash Flow Management

Investors can align withdrawals with recurring financial needs.

4. Flexibility

You can:

- Increase or decrease withdrawal amounts

- Change withdrawal frequency

- Pause or stop withdrawals

5. Reduced Risk of Overspending

A structured withdrawal approach helps preserve capital and promotes disciplined fund usage.

6. Potential Inflation Protection

Since only a portion of the investment is withdrawn, the remaining corpus continues to generate returns that may help combat inflation over time.

7. Planning withdrawals is only half the equation

A Systematic Withdrawal Plan can help generate regular income from your investments. But before you start withdrawing, it's equally important to understand how much wealth your investments could potentially build over time.

Who Should Consider an SWP?

An SWP can be suitable for various investor profiles.

Retirees

Retirees often require regular income after their salary stops. SWPs can serve as a self-created pension stream.

Parents

Parents can use SWP payouts to cover:

- School fees

- Tuition expenses

- Higher education costs

Loan Borrowers

Regular withdrawals may help manage EMIs and other recurring financial obligations.

Individuals Seeking Additional Income

SWPs can supplement primary income and support lifestyle goals.

SWP vs Lump Sum Withdrawal

Many investors face the dilemma of choosing between a lump sum redemption and an SWP.

Parameter | Lump Sum Withdrawal | SWP |

Entire corpus redeemed | Yes | No |

Regular income | No | Yes |

Market participation continues | No | Yes |

Risk of spending entire amount | Higher | Lower |

Income predictability | Limited | High |

For long-term financial sustainability, many investors prefer the systematic approach offered by SWPs.

SWP vs SIP

Although both strategies are systematic, their objectives are different.

Feature | SIP | SWP |

Purpose | Wealth Creation | Income Generation |

Cash Flow Direction | Into investments | Out of investments |

Best For | Working professionals | Retirees and income seekers |

Goal | Build corpus | Utilise corpus |

Many investors use SIPs during their earning years and later switch to an SWP during retirement.

Taxation of SWP

Taxation depends on:

- Investment type

- Holding period

- Applicable tax regulations

One important aspect of SWP taxation is that only the capital gains portion is taxed. The principal component of the withdrawal is generally not taxable.

Since tax laws may change periodically, consulting a qualified tax professional before initiating withdrawals is advisable.

Using an SWP Calculator

Planning withdrawals accurately is important to ensure that your corpus lasts as long as intended.

An SWP calculator helps estimate:

- Monthly withdrawal amount

- Remaining corpus value

- Expected investment growth

- Sustainability of withdrawals

For investors evaluating long-term financial plans, using an SWP calculator before starting withdrawals can provide valuable insights.

Similarly, those exploring insurance-linked wealth creation solutions can use a ULIP Calculator to estimate potential fund value and future withdrawal possibilities.

SWP from Life Insurance Plans

Although SWPs are commonly associated with mutual funds, many investors are unaware that certain life insurance products also offer similar withdrawal facilities.

ULIPs and SWP Features

Unit Linked Insurance Plans (ULIPs) combine:

- Life insurance protection

- Market-linked investment opportunities

Many modern ULIPs allow partial withdrawals after the mandatory lock-in period, enabling policyholders to create an income stream similar to an SWP.

Benefits of SWP Through ULIPs

- Regular income after the lock-in period

- Continued participation in market-linked funds

- Life insurance protection

- Goal-based financial planning

- Potential wealth creation alongside income generation

For individuals seeking both protection and investment growth, ULIPs can provide an effective framework for systematic withdrawals.

Before investing, it is useful to evaluate projected returns using a ULIP Calculator, which helps estimate future fund values and withdrawal potential based on investment assumptions.

Important Factors to Consider Before Starting an SWP

Before implementing an SWP strategy, consider the following:

Assess Income Requirements

Estimate monthly expenses accurately to avoid excessive withdrawals.

Keep Inflation in Mind

Future expenses may rise over time, requiring periodic review of withdrawal amounts.

Maintain an Emergency Fund

Avoid relying entirely on SWP withdrawals for unexpected expenses.

Review Portfolio Performance

Monitor investments regularly to ensure withdrawals remain sustainable.

Align With Financial Goals

The withdrawal strategy should support both current income needs and future financial objectives.

Is SWP the Right Choice for You?

An SWP may be suitable if you:

- Need regular income from investments

- Want to avoid withdrawing your entire corpus at once

- Prefer a disciplined withdrawal strategy

- Wish to remain invested in market-linked instruments

- Are looking for supplementary retirement income

However, the suitability of an SWP depends on individual financial goals, risk appetite, and investment horizon.

Conclusion

Understanding the systematic withdrawal plan is essential for anyone seeking a structured way to generate income from investments. An SWP allows investors to withdraw funds periodically while keeping the remaining corpus invested, offering a balance between liquidity and growth potential.

Whether used through mutual funds or through modern life insurance solutions such as ULIPs, an SWP can help create a predictable income stream without completely depleting your investments. With careful planning, realistic withdrawal expectations, and regular portfolio reviews, a Systematic Withdrawal Plan can become an effective tool for long-term financial security and income management.

Before You Go

The difference between a comfortable retirement and a stressful one often comes down to whether your money continues growing while supporting your income needs. A well-planned investment strategy can help you create wealth, generate regular income, and protect your family's future at the same time.

See how your investments could grow over the years and what they may be worth when you need them most.