When someone you love passes away, one of the most overwhelming emotions that you feel is grief. And grief can make everything else seem insignificant. However, it is important to remember, that the passing away of a loved one has more than emotional consequences. It also requires some necessary financial considerations.

Now, in moments and situations of grief, dealing with financial and legal matters may seem like another burden on your already tired soul. However, taking small, steady steps can help protect the family’s financial well-being in the long run.

To help you out, here’s an easy guide on the financial aspects that need to be taken care of in the first few days and weeks after the demise of a loved one. The goal here is simple: to help you take care of some essential activities in a manageable way, while giving yourself space to grieve.

Taking a Moment: Prioritising Essential and Immediate Expenses

After the demise of a loved one, it is important to make a note of some payments that need attention sooner, such as:

Medical bills that are unpaid

Funeral and cremation expenses

Utility bill payments/rent/EMIs to avoid penalties.

If finances feel tight during this time, remember that you do not have to manage everything at once. You can speak to the hospital and ask if they can offer a reduced settlement or be okay with instalments for the final medical bills. You can also speak to the bank if EMI payments are becoming difficult. Some banks may allow temporary relief when the family is going through a difficult time.

The First Few Days: Focusing on the Essentials

Once you have taken care of immediate expenses, you will need to channel your energies to get some important tasks done.

-

Obtaining the Death Certificate

A death certificate is the most crucial document you will need. Almost every financial process, such as a bank withdrawal, insurance claim, pension request, and property transfer, will ask for it. You can apply for it through the hospital or the local municipal authority.

Remember to request multiple original copies (10–15), as many institutions will likely require originals.

-

Informing Key Individuals

Employer: If the deceased person was employed at an organisation, inform their employer. This will help initiate the processing for the encashment of final salary and leaves, Provident Fund (PF) benefits, any gratuity payouts, and group insurance, if applicable.

Important Financial Institutions: Inform life insurance providers and banks. Explain your situation to the bank and request that theyem t mark the account as ‘Deceased’. If you held a joint account with your loved one, you may be allowed to continue using the same account. If you feel overwhelmed, know that it is okay if you only notify these institutions and not dive deep into the procedures. You do not have to fill out forms or raise a claim right away.

Remember, you can do things slowly. Most institutions may understand and let you take the time to get things done.

Small Steps Ahead: Collecting Important Documents and Personal Records

In the next few days, if your time and energy allow, consider initiating the process of gathering additional documents. You will require them to manage financial accounts and claims. You do not need to look for everything in one go. Do things gradually or ask a trusted family member to help.

Some documents you should search for include:

Aadhaar / PAN of the deceased- for identity verification.

Nominee / Legal heir ID proofs - For banks and/or the insurance company to process claims and account changes

Bank details - for transferring funds, if needed

Insurance policy copy/policy number - to initiate insurance claims.

PF/EPF account details - to claim for retirement benefits.

Will/succession papers (if any) - These are some of the most important documents, as they will determine who will inherit the deceased’s money and other assets.

Going Forward: Notifying Financial Institutions and Securing Accounts

When you are ready, you can take the next step, which is to notify all the financial institutions the deceased was associated with.

These can include:

Mutual fund companies

Stock-brokers/DEMAT account providers

Post office, if savings were held there

Cryptocurrency wallets or exchanges

As a nominee in any of these accounts, you have the right to claim or transfer these holdings.

It is completely alright if you do not understand some of the financial terms. You can reach out to the concerned institutions, and they will explain the process at a calm pace.

-

Cancel or Close Unnecessary Accounts

When you get the time, take a moment to cancel:

Credit cards

Subscriptions

Auto-pay services or payment mandates.

Moving Ahead: Initiating Claims for Benefits You Are Entitled To

In the days and weeks that follow, you can start the process of claiming any benefits meant for you and your family.

-

Raising a life insurance claim

As the beneficiary of your loved one’s term insurance plan, you can start the process of claiming the life insurance death benefit. Most insurers have a simple claim settlement process.

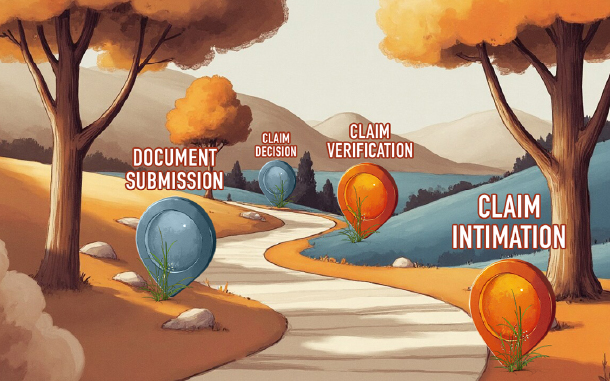

The process below provides some information on how to claim the life insurance:

Contacting the insurance company (visit their website or branch)

Filling out the claim form.

Submitting documents, such as the death certificate, policy document (or policy number), the deceased’s ID details, your ID and bank details, and more.

Once the claim is verified, the insurance company will typically settle the claim smoothly in a short time.

Remember, doing this can ensure that the efforts carried out by your loved one, in buying the policy and diligently paying the premiums, can provide financial support to you and your family during a difficult time.

-

Claiming PF, Pension, and Gratuity

If your loved one was employed, you may also be eligible to receive provident fund benefits, pension support, or gratuity. The company’s HR department can guide you through these steps.

-

Other Accounts and Deposits

If you are the nominee for a savings account, fixed deposit, or any other deposit/investment account, you will need to provide:

Death certificate

Claim form

Identity proof

Other documents, as deemed relevant by the institution.

In Closing

Financial matters might be the last thing on your mind when your loved one is not around. But it is important to take a small step towards a financially stable future. Taking one step at a time can make the journey gentler. Let each day unfold at a pace that feels right for your mind and heart. You are doing the best you can, and that is always enough on your part.